Make your plan work for you

We know staying healthy and having access to the best doctors matters — so does doing it affordably.

Annual Benefits Enrollment is your opportunity to choose from our variety of health plans offering comprehensive care, all designed to meet your needs without spending more than you need to.

Annual Benefits Enrollment for 2026 is October 6-24, 2025.

Understanding the plan terms and specifics

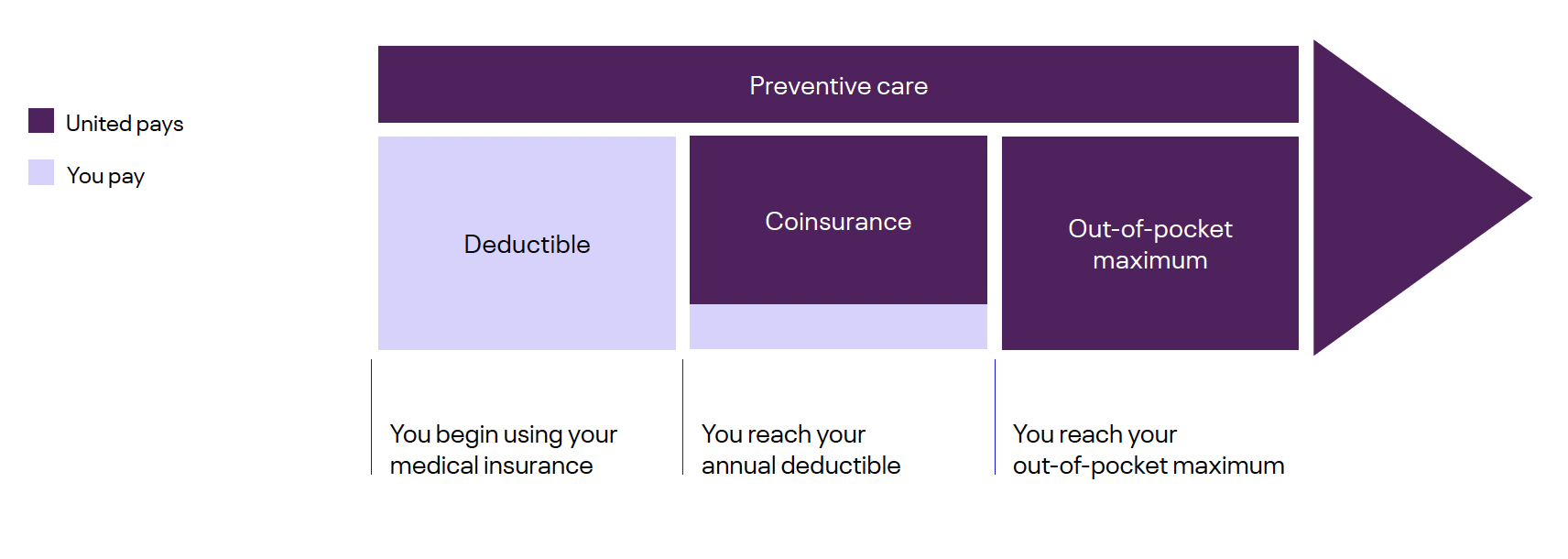

Deductible

The amount you are responsible for paying before the plan begins to pay a percentage of covered expenses. Typically, if you select a higher deductible plan, it means you’ll pay a lower monthly premium.

Coinsurance

The percentage you pay for covered services or prescription drugs after you have met your deductible.

Preventive care

Annual preventive visits and age-appropriate screenings are always covered at 100% for all plan options.

Out-of-pocket maximum

The most you’ll have to pay for covered medical expenses in a plan year; after you meet this amount, the plan will cover any additional eligible expenses at 100%.

Copay

A fixed amount you pay for covered services or prescription drugs, typically at the time you receive the services.

Premium

The amount you pay per month for your health insurance plan. You continue to pay the premium even after you’ve met your deductible.

Who pays and when

Lyra, mental health and Employee Assistance Program (EAP)

United has partnered with Lyra Health to offer all United employees comprehensive mental health and EAP services. Lyra offers 24/7 access to self-care tools, no-cost therapy and mental health coaching sessions to you, your spouse/qualified domestic partner and your dependents.

With Lyra, you have:

- Access to a care navigator for individualized treatment coordination on your mental health journey

- Eight (8) confidential and complimentary coaching and/or therapy sessions for you or your eligible family members, including evening and weekend availability to fit your schedule

- Access to on-demand resources for managing stress, improving sleep and strengthening relationships as well as financial/legal support and other professional consultations

- Care for the whole family, as Lyra’s Coaching for Parents program connects caregivers with specially-trained parent coaches to help navigate challenges like tantrums, picky eating, sleep issues, arguments, technology use and more

- Specialized providers for children and teens to receive age-appropriate and compassionate care. Teens also have the option to utilize digital self-help resources, educational content and book their own appointments

Services offered through Lyra are available now. Visit lyrahealth.com/united.

For more information about Lyra and other benefits available through Wayfinder, go to YBR > Flying Together> Employee Services> Wellness-Physical, Emotional and Financial (Wayfinder).

![]()

Maven, women’s and family health benefits

Maven is a flexible women’s and family health solution that delivers in-depth care from family planning through midlife.

With Maven, you have:

- All-inclusive virtual access to doula support for labor and delivery

- 24/7 connectivity to doulas who are ready to answer questions and support expecting mothers and families

Services offered through Maven will be available starting January 1, 2025.

For more information about Maven, go to mavenclinic.com/join/UnitedAirlines.

Why an HSA might be the way to go:

An HSA (Health Savings Account) is a tax-advantaged savings tool you can use to pay for covered medical expenses. You are responsible for your deductible and coinsurance up to the out-of-pocket maximum, but HSA dollars can help cover these costs. This option is specific to the United Savings PPO, Kaiser HMO HSA and Core HDHP.

Some of its many benefits include:

Low premiums

No "use it or lose it" rule for money in your HSA account

Triple-tax savings, as long as you use your HSA for eligible healthcare expenses

Funds roll over from year to year, and the money is yours to keep even if you leave United or retire

You can change how much you contribute to your HSA via payroll deductions at anytime

Automatic Critical Illness Insurance is included in the United Savings PPO

Earning wellness incentives up to $800 for individuals, $1,600 for families after you receive your annual physical by the deadline ($750/$1,500 is automatically funded if enrolled in the Core HDHP plan)

A few ways you might use an HSA:

If you’re anticipating a big healthcare expense in the future, such as having a baby, an HSA is a good strategy for setting aside money, so you don’t have to worry about unexpected expenses later.

If you were previously spending $300 a month on your monthly premiums, but the United Savings PPO has reduced that amount to $200, you can apply your monthly savings to your HSA to offset your deductible or out-of-pocket costs on a pre-tax basis.

No “use it or lose it” rule for money in your HSA account. If you plan on changing jobs or using the money next year, your HSA will always be there. It is a rollover account, which means unused funds are never lost and are tax-deferred.

How Flexible Spending Accounts (FSAs) can help you save:

An FSA provides you with a tax-free way to set money aside and pay for healthcare expenses that are not covered under the medical, dental or vision plans and/or pay for dependent care expenses.

How it works: FSAs allow you to contribute a portion of your salary to:

A “general-purpose” Health Care FSA (HCFSA) can be used to reimburse you for eligible healthcare expenses, such as medical, dental, and vision expenses. If you enroll in a health plan other than the United Savings PPO, Kaiser HSA HMO or Core HDHP, you will be eligible to contribute to a limited-purpose HCFSA for 2026.

A “limited-purpose” Health Care FSA (HCFSA) can only be used to reimburse you for eligible healthcare expenses for certain unreimbursed dental and vision services. If you are enrolled in the United Savings PPO, Kaiser HSA HMO or Core HDHP, you will be eligible to contribute to a limited-purpose HCFSA for 2026.

A Dependent Care FSA can be used to reimburse you for qualifying childcare and other dependent care expenses.

A few things to keep in mind with FSAs:

If you decide to contribute to an FSA, your contributions will automatically be made on a pre-tax basis from your paycheck and deposited in your FSA account.

After you elect to contribute to an FSA, your total annual contribution for the year will be divided into payroll deductions among the remaining payroll periods for the 2026 calendar year.

The maximum annual amount you may contribute to each FSA varies each year and is determined by the IRS.

Only the employee may enroll in an FSA, but you may submit eligible expenses you have incurred for care provided to your eligible dependents for reimbursement from your FSA.

You will be reimbursed for eligible healthcare and dependent care expenses that you have incurred upon your submission of a claim for reimbursement, along with the required documentation.

The entire amount of your annual contribution election to your Health Care FSA (reduced by previous reimbursements) is available to you at all times during the calendar year. You may submit a claim for reimbursement of a healthcare expense even if you have not yet contributed enough to cover the entire amount of the claim submitted.

Your Dependent Care FSA is limited to the amount you have contributed to date. If you have expenses greater than the amount accumulated in your Dependent Care FSA, they will be reimbursed automatically as additional contributions are credited to your FSA and you do not need to resubmit your claim.

All FSA accounts have a “use it or lose it” rule — funds don’t roll over from year to year. Any unused balance at the end of the plan year is forfeited, so be sure to use your funds before the year ends.

What’s yours with Wayfinder

Your health and well-being matter — and our commitment goes beyond the doctor’s office. Through resources like Wayfinder, United continues to be your home for tools and programs to help with everything from cost savings, to prescriptions, to wellness and more.

-

Accolade is your first point of contact for healthcare needs, from finding a primary care doctor, to managing a chronic condition, or helping to sort through medical bills.

*Access to this program is determined by your plan enrollment

-

Work with a certified financial coach to help with budgeting, debt management, saving and investing.

*Access to this program is dependent on your retirement plan enrollment. Only employees with an account balance in the United Airlines 401(k) Savings Plan or United Airlines Flight Attendant 401(k) Plan are eligible to participate in the LearnLux financial wellness program.

-

Access the country’s top hospitals and surgeons and get most, if not all, surgery costs covered including replacement or non-replacement of hip, knee, shoulder, spinal procedures, bariatrics and more.

*Access to this program is determined by your plan enrollment

-

Overcome joint and muscle pain through personalized online exercise programs tailored to your condition. You’ll also have unlimited access to a personal health coach.

*Access to this program is determined by your plan enrollment

-

Access diabetes reversal treatments that can help you get off diabetes medication, lose weight and reduce blood sugar.*Access to this program is determined by your plan enrollment

-

Connect to a leading specialist for a virtual second opinion on a diagnosis or treatment plan.

*Access to this program is determined by your plan enrollment

-

Access mental health coaching, therapy and self-help resources like meditations, videos and on-demand courses.

-

Connect with primary care providers offering same-day access via telehealth for primary, urgent and chronic care needs.

*Access to this program is determined by your plan enrollment

-

Start, continue and manage your 401(k) plan with access to trusted Fidelity advisors.

*Access to this plan is dependent on your workgroup.

-

Connect with a dermatologist who can guide you through an at-home skin cancer screening.

*Access to this program is determined by your plan enrollment

-

Access a flexible women’s and family health solution that delivers in-depth care from family planning through midlife.

*Access to this program is determined by your plan enrollment

Here’s an example of how Wayfinder works:

- Imagine your doctor recommends knee surgery.

- Log in to Wayfinder and select the Surgery tile to explore resources and support available before your procedure, including programs like Carrum Health.

- Carrum Health gives you access to some of the country’s top hospitals and surgeons, with most (if not all) surgery costs covered. Experts can guide you through your diagnosis, review alternative treatment options, and help you make a more informed decision.

Be sure to take a few minutes after January 1, 2026, to explore Wayfinder and discover the quality programs available to support your well-being.

Remember: Your interactions with third-party vendors through Wayfinder are not tracked by United. You can access vendor web pages, call them directly, and obtain vendor services with peace of mind that your personal information is secure and confidential.

Important dates to remember

Timeline for enrollment:

| 9/29 | Decision Guide and "Price & Compare" tool available on YBR |

| 10/6 | Enrollment begins |

| 10/24 | Enrollment ends |

| 01/01 | Your 2026 benefits begin |